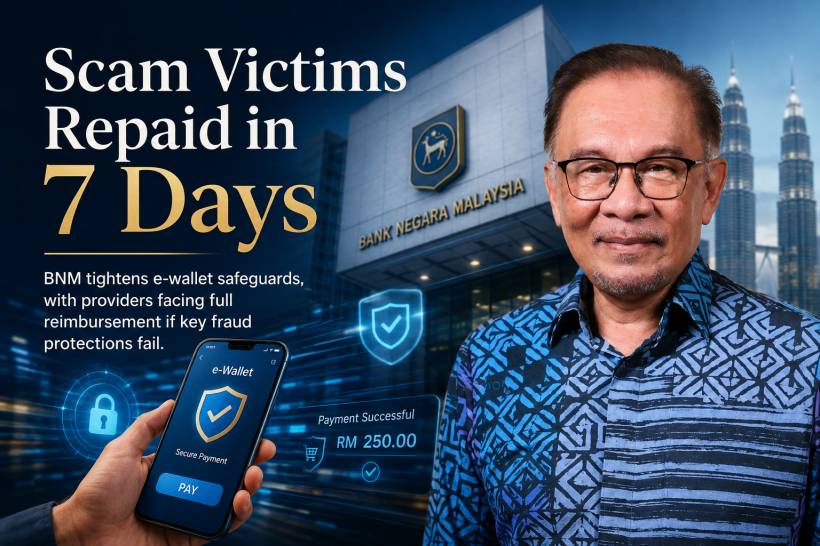

Malaysians who lose money through e-wallet scams may receive stronger protection under Bank Negara Malaysia's consumer-protection framework. E-wallet providers that fail to implement required fraud safeguards could be expected to fully compensate affected users within seven working days, according to a written parliamentary reply by Prime Minister Datuk Seri Anwar Ibrahim.

The policy is significant because it places clearer responsibility on payment providers, rather than leaving scam victims to carry the full burden of a loss when a provider has not put reasonable controls in place.

Compensation Can Still Apply Even When Users Made a Mistake

Scam cases are often complicated. Victims may have clicked a fraudulent link, shared a verification code, approved a transaction under pressure or been manipulated into transferring money themselves.

Under the framework described in Parliament, compensation can still apply even where the customer's own negligence contributed to the loss. The outcome is assessed based on the level of responsibility held by both the financial institution and the user.

That does not mean every scam loss will automatically be refunded. Instead, providers are expected to investigate whether proper security measures, fraud detection processes and customer safeguards were in place at the time of the incident.

What Safeguards Are Expected From Providers?

Banking institutions and eligible e-money issuers are expected to implement multiple layers of anti-fraud protection. These include stronger transaction authentication, cooling-off periods for higher-risk activity, account access tied to a single registered device, dedicated fraud hotlines and a "kill switch" function that allows customers to freeze access quickly when fraud is suspected.

These controls are designed to reduce the damage caused when scammers gain access to an account or persuade a victim to make a transfer. For example, a cooling-off period may give a customer time to recognise a suspicious transaction, while device binding can make it harder for fraudsters to take over an account from an unfamiliar phone.

Faster Scam Reporting and Fund Freezing

Malaysia has also strengthened the wider response system through the National Scam Response Centre and the National Fraud Portal. The portal is intended to automate parts of the reporting, fund-tracing and suspicious-transaction freezing process so action can be taken faster after a scam is reported.

Speed matters greatly in financial scams. Once stolen money is moved between multiple accounts, withdrawn or converted into other forms, recovery becomes much harder.

BNM advises scam victims to immediately contact their bank's scam hotline or call the National Scam Response Centre at 997, then lodge a police report.

An Independent Review Is Available

Customers who disagree with a bank's decision on compensation may seek an independent review through the Financial Market Ombudsman Service. This gives consumers another avenue when they believe an investigation or reimbursement outcome was unfair.

The framework is intended to improve accountability across banks and digital-payment providers while giving consumers a clearer path when fraud occurs.

A Growing Focus on Digital Payment Safety

As e-wallets, online banking and instant transfers become part of daily life, scam protection is becoming just as important as convenience. Anwar said enhanced security controls helped financial institutions prevent RM1.2 billion in fraudulent transactions last year, while the number of victims receiving full or partial compensation rose by 26% after the policy was fully implemented.

The message is increasingly clear: digital-payment providers are expected to do more than process transactions. They must also provide meaningful safeguards, respond quickly when fraud occurs and take responsibility when poor controls contribute to a customer's loss.

Final Thoughts

The proposed seven-working-day compensation requirement could offer important reassurance to e-wallet users, especially as scams become more sophisticated and harder to spot.

Users must still remain cautious with unexpected messages, links and payment requests. However, stronger obligations for providers recognise an important reality: fraud prevention is not only the customer's responsibility. Payment platforms must also have the systems, controls and response processes needed to protect the people who rely on them.

Comments