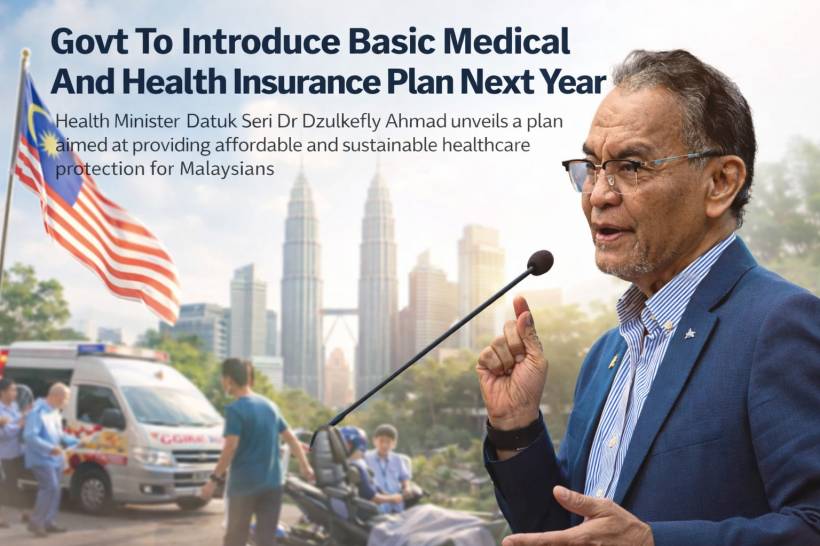

If you've ever tried comparing medical insurance plans and ended up more confused than confident, you're not alone. That's exactly the problem the government says it wants to tackle with a new baseline product: a basic Medical and Health Insurance/Takaful (MHIT) plan that's meant to be affordable, standardised, and easier to understand, while also helping to cool down the pressure from rising private healthcare costs.

The plan was unveiled in a joint announcement led by the Health Minister, alongside Finance Ministry II and Bank Negara Malaysia leadership, which is a strong hint that this isn't just "another insurance product". It's being framed as part of a broader effort to reshape how private healthcare financing works in Malaysia.

The price range people will immediately pay attention to

The base MHIT plan is expected to start at around RM80 to RM120 a month. That's an early pricing range, but it sets the tone: the plan is being positioned as a realistic entry point for people who want protection without committing to premiums that keep creeping up until they become impossible to justify.

When it's happening: pilot first, then rollout

The approach is staged:

That "pilot-then-rollout" structure matters because it suggests the government expects to test the mechanics (pricing, claims flow, sustainability, uptake) before pushing it nationwide.

What the "base" MHIT plan is meant to cover

This plan is designed as a standardised hospitalisation policy that focuses on major hospital bills, using shared-room costs as the reference point. In plain terms, it's trying to cover the type of hospital expenses that can wipe out savings, while keeping the baseline anchored to a more typical ward setting so the overall plan stays affordable.

It also isn't just about the hospital stay itself. The announcement says the base plan includes expanded pre- and post-hospitalisation benefits, such as:

The logic here is straightforward: people don't only incur costs during admission. The expenses often continue before admission (consultations, tests) and after discharge (rehab, follow-ups, home care). This plan is trying to acknowledge that reality.

Limits and protection: no lifetime limit, and an annual limit set for "most cases"

Two points stand out:

That structure is basically saying: this is intended to handle typical real-world hospital situations for most people, without being an unlimited product that becomes financially unstable.

Who can sign up, and how long it can stay active

Eligibility is also clearly defined:

This is important because one of the biggest anxieties around medical coverage is not just getting it, but keeping it as you age. Guaranteed renewal (to the stated age) is meant to reduce the fear of losing coverage right when healthcare needs tend to increase.

High-cost treatments like cancer: included, but with a sustainability filter

The plan includes high-cost areas such as inpatient and outpatient cancer care and related drugs, but coverage is described as being based on cost-effectiveness assessments.

In a conversational sense, this is the government trying to balance two competing needs:

And for those who need more coverage than the base provides, the structure allows for higher annual limits with higher premiums.

Why "standardised across insurers" is a bigger deal than it sounds

One of the most practical features is that benefits and premiums under the base MHIT plan will be standardised across insurers and takaful operators.

If that's implemented properly, it could reduce the usual headaches people face when shopping for medical coverage:

This is also why Bank Negara Malaysia's white paper frames it as a voluntary baseline product for the market, not just a one-off scheme.

The bigger reform angle: affordability, premium stability, and value-based care

The base MHIT plan is being positioned as part of a wider healthcare financing reform aimed at:

One example mentioned is the phased implementation of diagnosis-related group (DRG) payment models, which is essentially a more structured way of paying for care based on diagnosis categories, rather than letting costs drift unpredictably depending on how services are billed.

A new health insurance calculator is coming too

Alongside the MHIT initiative, the government and industry players are working on a health insurance and takaful calculator to help Malaysians plan long-term healthcare spending.

The idea is to let consumers estimate:

No timeline was given for when it will be available, but the intent is to make planning less guesswork and more math.

More price transparency at private hospitals

As part of broader transparency efforts, the industry has also published price ranges for 26 common medical procedures at private hospitals, showing:

This is meant to help people understand what "common procedures" might actually cost before they're stuck making decisions under pressure.

What Malaysians should take away from this

If the base MHIT plan launches as described, it could become the "default starting point" for medical coverage in Malaysia: a baseline that's easier to compare, designed to cover the majority of typical hospitalisation scenarios, and priced to be within reach for more households.

The bigger message, though, is that the government is trying to reshape the private healthcare financing conversation from "premiums keep going up" to "let's build a stable baseline and make the market easier to navigate."

Comments 0