TNG Digital has reached an important milestone in its journey from a payment-focused e-wallet into a broader digital financial services platform. The company, best known as the operator of TNG eWallet, recorded its first full-year profit since the e-wallet was launched in March 2018. For a platform that started mainly around payments, toll convenience, and cashless transactions, this marks a significant shift in how the business is now generating value.

The bigger story is not only that TNG Digital became profitable. It is how the company achieved that turnaround. For the first time, half of its revenue came from services beyond payments. These include financial services such as wealth management, insurance, remittance, lending, and business-to-business offerings. Compared with basic payment transactions, these areas generally offer better margins and give the company more room to grow sustainably.

Why This Profit Milestone Matters

E-wallet businesses are not easy to monetise. Payments may bring large transaction volumes, but the margins are usually thin. In some cases, payment services are offered more to keep users engaged than to generate strong profit on their own. This is especially true for QR payments involving small businesses, where the cost of supporting the ecosystem can be high while the income earned per transaction remains low.

That is why TNG Digital's shift into non-payment services matters. The company is no longer depending only on payment volume to grow. Instead, it is using its large user base as a foundation to offer more valuable services. Once users already trust the app for everyday payments, it becomes easier to introduce them to other financial products and lifestyle features.

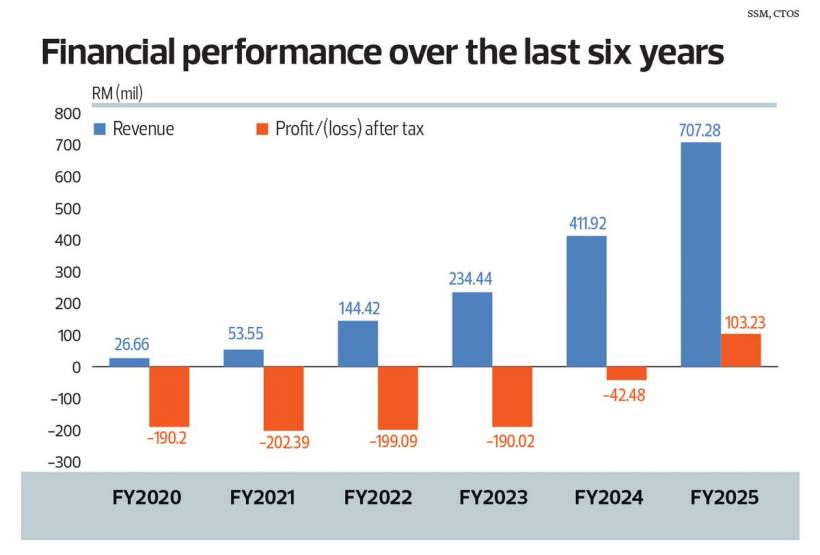

According to the company's financial filings, TNG Digital made a profit after tax of RM103.23 million for the financial year ended Dec 31, 2025. This reversed a loss after tax of RM42.48 million in the previous year. Revenue also rose strongly to RM707.28 million, up 72% from RM411.92 million the year before.

Payments Remain The Foundation, But Not The Whole Business

TNG Digital CEO Alan Ni described payments as the company's "home base". That is a good way to look at it. Payments may not always be the most profitable segment, but they are what keep users coming back to the app. People use the wallet to pay at merchants, make online payments, transfer money, handle cross-border transactions, and complete daily digital payment tasks.

The payments business itself reportedly broke even for the first time last year, which is a major achievement considering the scale needed to offset its thin margins. But TNG Digital is clear that payments alone are not where most of the company's future profit will come from.

The more meaningful growth is coming from cross-selling. When users already rely on TNG eWallet for payments, the company can introduce them to financial services, remittance, cross-border payment tools, insurance, lending, and B2B services. These areas are becoming increasingly important because they provide stronger margins than basic payment processing.

A Huge Verified User Base Gives TNG Digital An Advantage

One of TNG Digital's biggest strengths is its scale. The company now has 26 million verified customers, all of whom have gone through electronic know-your-customer verification. Of that number, 23 million are Malaysians, representing more than 85% of Malaysia's adult population.

That is a massive distribution advantage. Many financial service providers spend heavily to acquire customers, build trust, and encourage users to try their products. TNG Digital already has a large user base inside one app. This makes it attractive as a platform for banks, insurers, lenders, and other partners that want to reach Malaysian consumers more efficiently.

In simple terms, TNG Digital does not need to become a bank to offer banking-related products. It can work with licensed partners, distribute their products through its app, and earn commission income from that activity.

The Partnership Model Behind Its Growth

One of the most interesting parts of TNG Digital's business model is that it does not carry every financial product on its own balance sheet. Instead, it partners with financial institutions and other companies to offer services through its platform.

Its financial services now cover areas such as wealth management, insurance, remittance, and lending. Partners include CIMB Group, Alliance Bank Malaysia, and other institutions. This allows TNG Digital to expand quickly without needing to build every product, licence every service, or operate like a full bank.

This model makes the app more like a large distribution platform. Users can access financial services through TNG eWallet, while the underlying product remains with the partner. For TNG Digital, this keeps the business more flexible and less capital-heavy.

It also changes how the company views competition. Ni suggested that many competitors can also become partners. If another company has a strong financial product, TNG Digital can potentially work with them instead of trying to build the same thing from scratch.

From E-Wallet To Everyday Digital Companion

TNG Digital's ambitions now go beyond payments and financial services. The company appears to be moving toward becoming what it calls an "everyday digital companion". This means the app is being expanded to support more parts of daily life, not just payment transactions.

Users can already access features such as restaurant discovery, digital arrival card support for travel, and temporary toll coverage when their wallet balance is insufficient. Some of these features may not be directly monetised, but they help make the app more useful and keep users engaged.

This is where the company starts to look closer to a super app, although Ni is careful not to fully use that label. He noted that true super apps, especially those in China such as WeChat Pay, Alipay, and Meituan, have much wider ecosystems. Still, in the Malaysian context, TNG Digital may be one of the closest local apps to that direction.

The Cashless Shift Is Still Driving Growth

Malaysia's move from cash to cashless payments is still not complete. That ongoing shift continues to support growth in digital payments. As more merchants, consumers, and services accept QR and e-wallet payments, platforms like TNG eWallet remain highly relevant.

Ni also noted that Malaysia ranks very highly globally in QR code payment adoption, behind China. This shows how normalised QR payments have become in the local market. For TNG Digital, that is both an opportunity and a challenge.

The opportunity is obvious: more cashless behaviour means more usage. The challenge is that the market is crowded. Malaysia has many e-wallet players, while banks, digital banks, and fintech companies are also competing for the same users.

TNG Digital's Shareholders And Market Position

TNG Digital's largest shareholder is CIMB Group Holdings, which owns 45.01% through Touch 'n Go Sdn Bhd. Other shareholders include Ant International Technologies, Lazadapay Holdings, ASP Malaysia LP, and AIA Bhd.

This shareholder structure gives TNG Digital a mix of banking, fintech, digital commerce, investment, and insurance-linked backing. It also helps explain why the platform has been able to expand across payments, financial services, and ecosystem-based offerings.

Interestingly, toll and parking payments now contribute only a low single-digit percentage of TNG Digital's revenue. That may surprise many Malaysians who still associate the Touch 'n Go brand mainly with highways and parking. The toll and parking business is operated by Touch 'n Go Sdn Bhd, while TNG Digital receives fee-based income from certain related products such as RFID and PayDirect.

This shows how much the e-wallet business has evolved beyond its original association with toll payments.

Looking Toward RM1 Billion Revenue

TNG Digital's revenue has reportedly grown at a compound annual growth rate of about 70% over the past four years. The company is targeting RM1 billion in revenue for FY2026, and based on its current trajectory, it may exceed that target.

That growth will likely continue to come from a mix of payments, remittance, cross-border services, B2B offerings, and financial services. Lending is still a small part of the business, contributing around 3% to 4% of total revenue, but it is an area with room to grow.

The company is also exploring new lifestyle and family-focused features. One possible launch mentioned is a "family wallet", which would allow parents and children to link their e-wallets. TNG Digital has also launched TNG Digital Singapore, with usage expected to focus mainly on Singaporeans spending across the border in Johor.

Final Thoughts

TNG Digital's first annual profit is more than just a financial result. It signals that the company has entered a more mature phase. The early years were about building scale and getting Malaysians to use the app. The current phase is about monetising that scale through higher-margin services while keeping payments as the core engagement engine.

The challenge from here is no longer whether Malaysians know or use TNG eWallet. The bigger question is how deeply the app can become part of everyday life. Payments may have opened the door, but financial services, cross-border usage, lifestyle tools, B2B services, and future family-focused features may decide how far the platform can go.

For TNG Digital, profitability shows that the model is beginning to work. But in a crowded fintech and digital banking landscape, staying ahead will require more than a large user base. It will need useful services, trusted partnerships, strong execution, and a clear reason for Malaysians to keep returning to the app every day.

Comments