Malaysia has been attracting major attention as a digital investment destination. On paper, the story looks very strong. The country has secured RM342.58 billion in approved digital investments, with more than 114,000 projected jobs expected to be created. Even more importantly, most of those jobs are knowledge-worker roles, meaning they are linked to higher-value areas such as technology, digital services, finance, outsourcing, artificial intelligence and related business operations.

But there is one problem that may not sound exciting at first, yet could become a real bottleneck: Malaysia may not have enough certified, digitally ready office space to properly support this growth.

A joint whitepaper by Knight Frank Malaysia and Malaysia Digital Economy Corporation, or MDEC, has highlighted this issue clearly. The demand for digital business space is real. The investments are real. The jobs are real. But the supply of certified office buildings that meet modern digital, sustainability and operational expectations is still limited.

The Digital Economy Needs More Than Just Any Office

For many years, office space was mainly judged by location, rental rate, parking, building age and basic facilities. Those factors still matter, but they are no longer enough for serious digital economy tenants.

A company involved in artificial intelligence, fintech, Global Business Services, Knowledge Process Outsourcing or regional digital operations will usually look at a building very differently. They are not simply renting a few desks and meeting rooms. They need reliable power, strong digital infrastructure, proper connectivity, business continuity readiness, compliance support, good building management and increasingly, environmental certification.

This is why the office space issue matters. Malaysia is trying to attract and retain higher-value digital investors, but these companies often expect premises that match international standards. If there are not enough suitable buildings, the investment story becomes harder to fully convert into actual office demand.

In simple terms, Malaysia may have the digital investment momentum, but it also needs the right physical infrastructure to house that momentum.

The Certification Gap Is Quite Clear

The numbers from the whitepaper are telling. Only 13 percent of Malaysia Digital-status companies currently operate from MD-certified premises. Only 15 percent are located in green-certified buildings. Even more limited, just 10 percent occupy space that is both MD-certified and green-certified.

That means most Malaysia Digital companies are still operating outside the type of certified premises that would best match the country's digital economy ambitions.

The supply side also shows the same problem. Only 35 percent of existing purpose-built office stock in Malaysia is MD-certified. In the Klang Valley, green-certified buildings account for only 21 percent of purpose-built office stock.

This is why the issue should not be seen as a lack of demand. The demand is already there. The problem is that there are not enough buildings that can properly position themselves as suitable homes for premium digital economy tenants.

Why Foreign Digital Investors Are More Selective

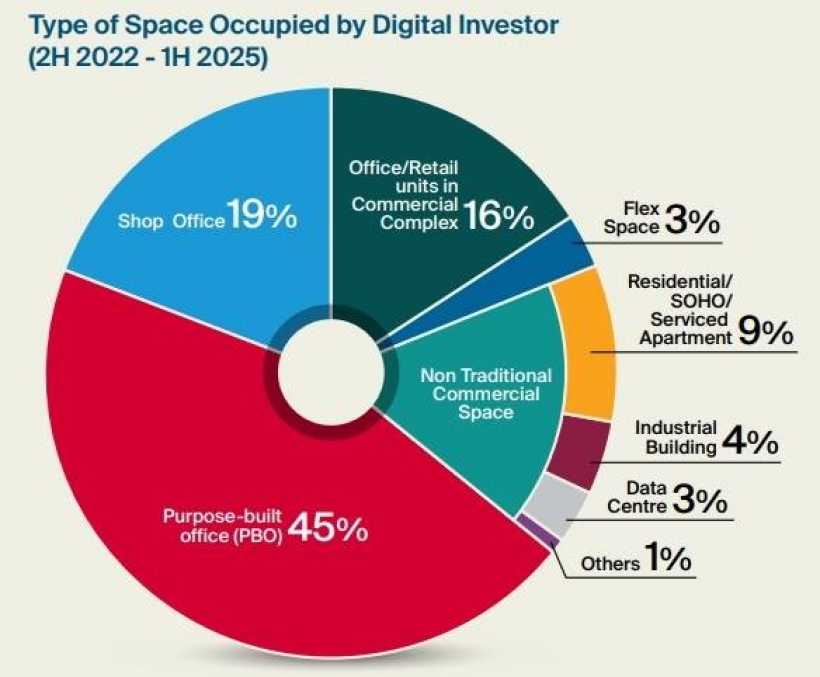

Foreign digital companies are a major part of Malaysia's investment story. According to the whitepaper, foreign digital firms account for 67.7 percent of Malaysia's approved digital investment value. These companies are also more likely to prefer purpose-built offices, with 55 percent of foreign Malaysia Digital firms operating from such premises.

This preference is not surprising. Foreign investors, especially larger multinational or regional technology companies, usually have internal requirements for compliance, cybersecurity, workplace quality, uptime, ESG alignment and operational resilience. They may also need to report to headquarters or global stakeholders on whether their office locations meet specific standards.

For these companies, a cheaper but older office building may not be attractive if it lacks digital readiness, sustainability certification or reliable infrastructure. They would rather choose premises that allow them to operate confidently, recruit talent more easily and satisfy internal governance requirements.

This is where certified buildings gain an advantage.

Knowledge Workers Raise The Standard For Office Demand

The projected jobs linked to Malaysia's digital investment pipeline are not mostly low-skilled or routine roles. A large share is expected to come from knowledge-worker positions. These workers usually operate in areas such as analytics, software, business process services, finance operations, digital support, artificial intelligence and other specialised functions.

This matters because knowledge-worker tenants tend to place higher importance on workplace quality. They are more likely to expect good connectivity, comfortable working environments, reliable facilities, collaborative spaces, convenient locations and modern building standards.

For landlords, this creates both an opportunity and a warning. Buildings that meet these expectations can attract better-quality tenants. Buildings that do not may gradually become less competitive, especially as newer certified offices enter the market.

Older office stock may still find tenants, but the gap between premium certified buildings and outdated non-certified buildings could widen over time.

GBS, AI And Fintech Could Drive Real Office Demand

Not all digital investments translate into office demand in the same way. Data centres, for example, can involve massive investment value but may be more land-, power- and infrastructure-intensive than people-intensive. By contrast, sectors such as Global Business Services, Knowledge Process Outsourcing, fintech and artificial intelligence can generate more office-based employment.

The whitepaper notes that Malaysia's mature digital clusters, including AI, GBS/KPO and fintech, show strong concentration in purpose-built offices. This is important because these sectors can create recurring demand for quality office space as teams grow.

GBS/KPO alone is highlighted as a major employment generator, with RM26.16 billion in approved investments and 39,428 projected jobs. That kind of job creation does not only affect the labour market. It also affects office demand, transport planning, surrounding retail activity and urban business districts.

If Malaysia wants to capture the full benefit of these investments, the country needs enough suitable office environments for these companies to scale.

MDLR Could Help Create A Clearer Path Forward

One important development is the Malaysia Digital Location Recognition framework, or MDLR, which came into effect on 1 January this year. This framework replaces the earlier MD Cybercity and Cybercentre model and introduces a more structured recognition system.

The framework has three tiers. MD Hub is aimed at startups and MSMEs operating in flexible or shared workspaces. MD Nexus is designed for premier business premises serving established digital investors. MD Tech Zone applies to purpose-planned digital technology development areas such as business parks.

This is a meaningful change because it gives property owners and developers a clearer certification pathway. The MD Nexus standard focuses on four key areas: digital infrastructure, electrical supply, vibrancy of the business environment and enhanced value proposition.

That makes the criteria easier to understand from a commercial perspective. Instead of certification feeling like a separate administrative exercise, it becomes more closely aligned with what digital occupiers are already looking for.

Merdeka 118 Sets An Early Benchmark

Merdeka 118 becoming the first building to receive MD Nexus recognition is significant because it gives the market a visible reference point. It shows what a premium digitally certified office building can represent in Malaysia.

The recognition is not just about having modern internet connectivity. It signals that the building is prepared for the expectations of digital investors, including infrastructure readiness, resilience and a more technology-enabled operating environment.

For high-value tenants, especially multinational digital companies, that kind of certification can reduce uncertainty. It helps them identify buildings that are more likely to meet operational and compliance expectations from the start.

Developers And REITs Have A Timely Opportunity

For developers, REIT managers and office landlords, this situation creates a practical investment opportunity. The office market is not just about adding more square footage. It is about adding the right kind of square footage.

The upcoming supply in Klang Valley, Johor and Penang is reportedly moving in the right direction, with many new projects being designed to be tech-ready and ESG-aligned. This should help reduce the certified space gap over time.

However, the more difficult question involves existing buildings. Many older Grade A and Grade B offices were built before ESG, digital readiness and tech-enabled operations became mainstream requirements. These buildings may still be physically usable, but they may not be competitive enough for future digital economy tenants without upgrades.

Owners of older office buildings may need to consider retrofitting, certification upgrades, better connectivity, improved energy efficiency, stronger building systems and enhanced tenant facilities. Otherwise, they risk losing tenants to newer buildings that already meet modern requirements.

A Two-Speed Office Market May Become More Obvious

Malaysia's office market could increasingly split into two categories. On one side, certified, green, digitally ready buildings may enjoy stronger demand from high-quality tenants. On the other side, older and non-certified buildings may face slower take-up, weaker rental growth or higher vacancy risk.

This kind of split is already visible in many major office markets around the world. Tenants are becoming more selective, especially after hybrid work changed how companies think about office space. If a company is going to maintain a physical office, it wants that office to provide real value.

For digital economy tenants, that value comes from infrastructure, talent attraction, sustainability, resilience and location quality. Buildings that cannot deliver these may find themselves competing mostly on price.

Final Thoughts

Malaysia's digital investment story is impressive, but investment approvals are only part of the equation. The next challenge is making sure the country has enough certified, sustainable and digitally enabled office space to support the companies and jobs that come with that investment.

The Knight Frank Malaysia and MDEC whitepaper makes the issue clear: this is not a demand problem. It is a supply problem. Digital investors are coming, and knowledge-worker jobs are expected to grow. But many of these companies will need office spaces that meet higher standards than traditional buildings can offer.

For developers, landlords and REITs, the message is straightforward. The future of office demand in Malaysia will not be won by simply owning space. It will be won by owning the right space.

Certified, green and tech-ready buildings are likely to become more important as Malaysia's digital economy matures. Those who upgrade early may be better positioned to capture the next wave of demand. Those who wait too long may find that the market has quietly moved on without them.

Comments 0